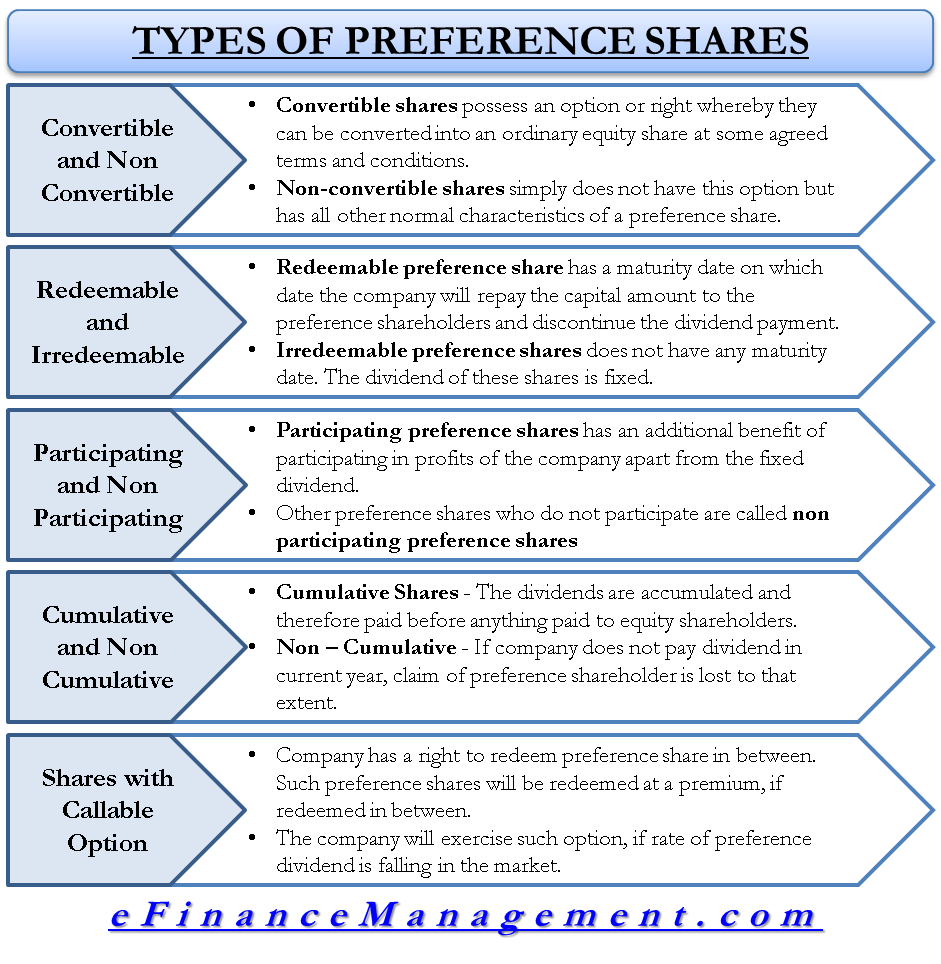

The $200,000 loan has an interest rate of 5% and is amortized over 10 years. Using a loan payment calculator, this comes to a total monthly payment of $2,121.31. CFI is the global institution current assets definition lists and formula 2023 behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path.

Example of Short/Current Long-Term Account

Double Entry Bookkeeping is here to provide you with free online information to help you learn and understand bookkeeping and introductory accounting. The Debt Service Coverage Ratio (DSCR) is one of banking’s favorite ratios. We’ve got some simple, no-fuss pointers that will help you nail this ratio every time. I’m Clay Sharkey, and there is nothing I like more than assisting others in achieving their goals. I firmly believe that by enhancing a banker’s understanding of their customer’s’ business, they can provide superior service. This superior service, in turn, leads to stronger relationships for the bank, improved performance for the businesses, and better experiences for our communities.

Create a free account to unlock this Template

In the notes to the financial statements the net amount of long term debt shown in the balance sheet would be explained as follows. Municipal bonds are debt security instruments issued by government agencies to fund infrastructure projects. Municipal bonds are typically considered to be one of the debt market’s lowest risk bond investments with just slightly higher risk than Treasuries. Government agencies can issue short-term or long-term debt for public investment. A business has a $1,000,000 loan outstanding, for which the principal must be repaid at the rate of $200,000 per year for the next five years.

The Financial Modeling Certification

Under IFRS Standards, no specific guidance exists when an otherwise noncurrent debt obligation includes a subjective acceleration clause. Classification of the liability is based on whether the debtor has an unconditional right to defer settlement of the liability at the reporting date. As observed in the graph above, the SeaDrill balance sheet doesn’t paint a good picture because its CPLTD has increased by 115% on a year-over-year basis.

- Classification of the liability is based on whether the debtor has an unconditional right to defer settlement of the liability at the reporting date.

- For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online.

- To address questions raised about applying these amendments to debt with covenants, the IASB Board published further proposals, including to defer the effective date of the 2020 amendments to January 1, 2024.

- A company can keep its long-term debt from ever being classified as a current liability by periodically rolling forward the debt into instruments with longer maturity dates and balloon payments.

- Each year, the balance sheet splits the liability up into what is to be paid in the next 12 months and what is to be paid after that.

This line item is closely followed by creditors, lenders, and investors, who want to know if a company has sufficient liquidity to pay off its short-term obligations. If there do not appear to be a sufficient amount of current assets to pay off short-term obligations, creditors and lenders may cut off credit, and investors may sell their shares in the company. The short/current long-term debt is a separate line item on a balance sheet account. It outlines the total amount of debt that must be paid within the current year—within the next 12 months.

How do accounts payable show on the balance sheet?

For example, startup ventures require substantial funds to get off the ground. This debt can take the form of promissory notes and serve to pay for startup costs such as payroll, development, IP legal fees, equipment, and marketing. Even though the loan isn’t paid off for many years, it still has a portion of the note that must be repaid each year. This is the current portion of the long-term debt– the amount of principle that must be repaid in the current year. Thus, the company has $0.50 in long term debt (LTD) for each dollar of assets owned. The rationale is that the core drivers are identical, so it would be unreasonable to not combine the two or attempt to project them separately.

Current liabilities are those a company incurs and pays within the current year, such as rent payments, outstanding invoices to vendors, payroll costs, utility bills and other operating expenses. Long-term liabilities include loans or other financial obligations that have a repayment schedule lasting over a year. Eventually, as the payments on long-term debts come due, these debts become current debts, and the company’s accountant records them as the CPLTD. Interested parties compare this amount to the company’s current cash and cash equivalents to measure whether the company is actually able to make its payments. Interested parties compare this amount to the company’s current cash and cash equivalents to measure whether the company is actually able to make its payments as they come due.

The current portion of long-term debt (CPLTD) refers to the section of a company’s balance sheet that records the total amount of long-term debt that must be paid within the current year. An analyst should attempt to find information to build out a company’s debt schedule. This schedule outlines the major pieces of debt a company is obliged under, and lays it out based on maturity, periodic payments, and outstanding balance. Using the debt schedule, an analyst can measure the current portion of long-term debt that a company owes. That’s why the current portion of long-term debt is presented with the other current liabilities on the balance sheet.